Q1 Market Commentary: A Look Back & Ahead

MODERNIST’S ASSET CLASS INVESTING PORTFOLIOS ARE STRATEGICALLY INVESTED WITH A FOCUS ON LONG-TERM PERFORMANCE OBJECTIVES. PORTFOLIO ALLOCATIONS AND INVESTMENTS ARE NOT ADJUSTED IN RESPONSE TO MARKET NEWS OR ECONOMIC EVENTS; HOWEVER, OUR INVESTMENT COMMITTEE EVALUATES AND REPORTS ON MARKET AND ECONOMIC CONDITIONS TO PROVIDE OUR INVESTORS WITH PERSPECTIVE AND TO PUT PORTFOLIO PERFORMANCE IN PROPER CONTEXT.

As evidence-based investors, we use an approach fueled by data with over 50 years of research, rooted in diversification, and tax conscious investment options. Time has proven the value of investing. While these quarterly market reviews are helpful for staying informed, we also love to remind our clients and community: focus on what you can control, remember the big picture, and stick to your plan.

market snapshot

After a calm start to the year, equities declined late in Q1 as investors weighed rising geopolitical risks. In the U.S., the S&P 500 turned negative in March after earlier record highs. Developed international and emerging markets outperformed, showing resilience despite Middle East instability.

U.S. and international fixed income posted modest gains, as income was offset by falling prices. Markets repriced a less dovish Federal Reserve outlook in 2026, pushing yields higher and weighing on bond prices.

Economic Spotlight:

What Does Geopolitical Conflict Mean for the Market?

Source: Focus Partners Wealth. “Geopolitical Conflict and Markets | A Brief History Lesson” March 2, 2026

History offers a helpful perspective. While geopolitical shocks create short-term uncertainty, the long-term behavior of markets has been remarkably consistent. Markets dislike uncertainty, so they often react quickly, but they also tend to recover faster than many expect. Over time, economic fundamentals have mattered far more than geopolitical headlines.

Recent conflicts illustrate this well. When Russia invaded Ukraine in February 2022, the S&P 500 initially declined from 4,288 to roughly 3,941 over three months, a drop of about 8%. This was a meaningful short-term reaction, largely because the conflict affected energy markets, supply chains, and inflation.

Looking more broadly, history shows a consistent pattern. Since World War II, geopolitical events have typically led to modest, short-lived market declines. According to LPL Research, the S&P 500 has fallen an average of about 5% following such shocks, usually bottoming within three weeks and recovering within one to two months.

This does not mean conflicts are irrelevant. Some have had lasting economic consequences. The 1970s oil embargo, for example, contributed to a prolonged period of inflation and weak market returns. More recently, the war in Ukraine added to inflation pressures already building in the global economy. But in each case, markets reacted primarily to the economic impact, not the event itself.

That distinction is critical. Markets respond to changes in growth, inflation, and corporate earnings—not simply the presence of conflict.

For investors, the takeaway is straightforward. Short-term volatility during geopolitical events is normal. But history suggests that making long-term investment decisions based on headlines has rarely been a successful strategy. In the moment, every crisis feels different.

History suggests most are not.

Geopolitical Tensions Take Center Stage Clouding Future Growth Outlook

Main Takeaway

The U.S. economy appeared to slow in Q4, expanding at a modest 0.7% (1) annualized pace. However, this understates underlying strength, as a 43-day government shutdown reduced GDP by roughly 1.0%–1.2%. Meanwhile, Middle East tensions have renewed inflation concerns via higher energy prices. The labor market showed some improvement, adding 205,000 jobs in Q1 (2), though growth has moderated on a year-over-year basis.

Top Risks

Geopolitical tensions in the Middle East continue to pressure the global economy, as elevated oil prices weigh on near-term growth. A prolonged conflict risks further slowing activity while reigniting inflation concerns. Meanwhile, policy uncertainty has increased after the Supreme Court struck down the Trump administration’s authority to impose unilateral tariffs. Consumer confidence also remains weak, with sentiment hovering near decade lows, underscoring a cautious outlook for both households and businesses.

Sources of Stability

Despite ongoing headwinds, the U.S. economy is still expected to grow at a 1.3% annualized rate in Q1 (3). Consumer spending remains resilient, particularly among higher-income households, rising 2.0% in Q4. Real-time indicators, including credit and debit card data from Bank of America, point to solid spending in February. While job growth has moderated in recent quarters, it remains positive, with unemployment holding steady at 4.3% (4), supporting overall economic stability.

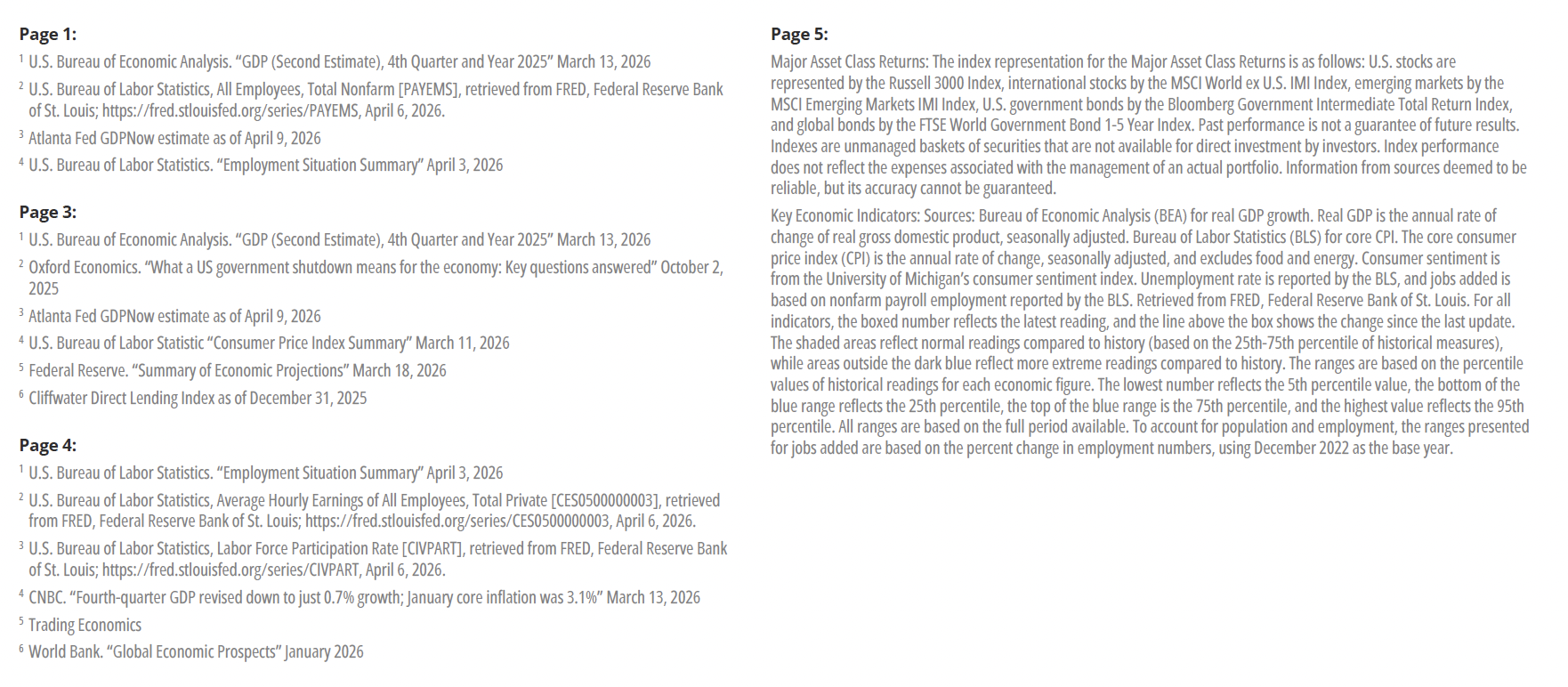

KEY ECONOMIC INDICATORS: AREAS TO WATCH

U.S. Economic Growth

U.S. economic growth slowed in Q4, rising at a 0.7% (1) annualized rate and bringing 2025 real GDP growth to 2.1%. This drop is somewhat misleading, as a 43-day government shutdown likely reduced growth by about 1.0%–1.2%. (2) Looking ahead, Q1 growth is projected near 1.3%3, with real final sales slightly higher at 1.4%. Overall, growth has cooled, and the outlook remains uncertain.

Inflation Trajectory

Inflation stayed above the Federal Reserve’s 2% target in February, largely in line with expectations. Headline and core CPI rose 0.3% and 0.2% (4) for the month, with 12-month rates at 2.4% and 2.5%. Inflation was broadly stable, as gains in shelter and services were partly offset by declines in goods like used vehicles and auto insurance. Headline CPI may rise near term as energy prices increase due to the Iran conflict.

Monetary Policy

The Federal Reserve held the federal funds rate at 3.50%–3.75% in January and March. Chairman Powell said the Middle East conflict’s impact remains uncertain, especially how higher oil prices may affect inflation expectations. The March “dot plot” (5) signals one rate cut in 2026, versus market expectations of none. This marks a shift from January, when two cuts were expected.

PRIVATE CREDIT

Recent headlines have raised concerns about stress in private credit, especially in software amid AI disruption. While worth monitoring, these risks may be overstated. About 70% of software borrowers saw positive EBITDA growth last year, versus roughly 50% overall. Defaults, non-accruals, and PIK usage remain at or below historical averages. (6) Private credit remains income-driven, with yield offsetting modest losses. Overall, fundamentals are stable and risks appear manageable.

Labor Market

March’s labor report showed a rebound, with 178,000 jobs added and unemployment at 4.3% (1), in line with its 12-month average. The first quarter saw total job growth of 205,000, a turnaround from the 116,000 jobs lost in Q4. However, beneath the headline, wage growth continued to slow in Q1 (2), extending a trend from late 2024, while the labor force participation rate (3) has also declined. Overall, the data suggests a labor market that remains healthy but is gradually cooling.

Consumer spending

Although still positive, consumer spending slowed in Q4, rising 2.0% (4), down notably from 3.5% in Q3. Looking ahead, Bank of America data shows debit and credit card spending increased in both January and February, with February marking the strongest usage in over three years. Despite this, the Atlanta Fed projects consumer spending to slow further to 0.9% for the quarter, reflecting higher near-term inflation and geopolitical uncertainty. Unsurprisingly, consumer sentiment remains near five-year lows.

Global Economy

Economic growth remained modest across Europe in Q4, with U.K. GDP rising just 0.1% (5) for a second consecutive quarter and the Euro Area expanding 0.2% (5). In contrast, Asia showed improvement, led by China at 1.2% (5) and Japan at 0.3% (5). Looking ahead, the World Bank forecasts global GDP growth of 2.6% in 20266. The U.S. is expected to grow 2.2%, while developed markets lag, with the Euro Area and Japan at 0.9% and 0.8%. Emerging markets are projected to lead with 4.0% growth.

tariff policy

On February 20, the Supreme Court ruled 6–3 that the International Emergency Economic Powers Act (IEEPA) does not grant the President unilateral authority to impose broad, indefinite tariffs. The decision immediately reduced the effective tariff rate from roughly 19% to around 9%–10%. In response, President Trump announced a new 15% global tariff, valid for 150 days pending Congressional approval, pushing the effective rate back to approximately 14%. This rapid policy shift has introduced renewed uncertainty into markets, which tends to weigh on investor confidence.

Thanks to our reliance on long-term evidence-based investing principals, we know that short term data is too noisy to determine our investing choices. Yet, we always like to offer our review of markets because we believe this information should be accessible to all!

Investment Planning Implications

Where do markets go from here?

Mag 7 struggles. The Magnificent Seven are off to a weak start, down 12.1% on average, led by declines in Microsoft (-23.3%), Tesla (-17.3%), and Meta (-13.3%). This may signal shifting sentiment as valuations normalize and investors demand clearer returns on heavy AI spending.

Value leads. Despite negative Q1 equity returns, value stocks held up well. In the U.S., both large- and small-cap value outperformed growth, with a similar trend internationally. With valuations still more attractive, value’s relative strength could continue if normalization persists.

Monetary policy uncertainty. The conflict in Iran adds to an already uncertain policy backdrop. Sustained tensions could keep energy prices elevated, slowing growth and complicating inflation. Fed funds futures reflect this shift, moving from pricing in two 2026 rate cuts in January to none by March

What are the investment planning implications?

Stay the course. The early March sell-off tied to the Iranian conflict is a reminder that volatility is both common and often sudden. Investors who react to headlines risk missing the recoveries that have historically followed market pullbacks.

Managing inflation risk. Ongoing Middle East tensions have pushed oil prices to multi-year highs, reviving inflation concerns. Allocating to real assets may help preserve purchasing power and provide some protection against rising prices over time.

Diversification matters. Volatility is an inherent part of equity investing. Incorporating differentiated return sources, such as alternative strategies, can help. Approaches like reinsurance and market-neutral investing often have low correlations with stocks and bonds, potentially improving diversification and portfolio stability, though they may not suit all investors.

For informational and educational purposes only and should be construed as specific investment, accounting, legal or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Indexes are unmanaged baskets of securities that are not available for direct investment by investors. Index performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Foreign securities involve additional risks, including foreign currency changes, political risks, foreign taxes, and different methods of accounting and financial reporting. Emerging markets involve additional risks, including, but not limited to, currency fluctuation, political instability, foreign taxes, and different methods of accounting and financial reporting. All investments involve risk, including the loss of principal, and cannot be guaranteed against loss by a bank, custodian, or any other financial institution.