Key Investment Themes to Watch in 2026

MODERNIST’S ASSET CLASS INVESTING PORTFOLIOS ARE STRATEGICALLY INVESTED WITH A FOCUS ON LONG-TERM PERFORMANCE OBJECTIVES. PORTFOLIO ALLOCATIONS AND INVESTMENTS ARE NOT ADJUSTED IN RESPONSE TO MARKET NEWS OR ECONOMIC EVENTS; HOWEVER, OUR INVESTMENT COMMITTEE EVALUATES AND REPORTS ON MARKET AND ECONOMIC CONDITIONS TO PROVIDE OUR INVESTORS WITH PERSPECTIVE AND TO PUT PORTFOLIO PERFORMANCE IN PROPER CONTEXT.

Markets fared better than feared in 2025, yet 2026 could continue to be uncertain. Strong earnings, tax benefits for consumers, and AI-related productivity gains could help position the economy for continued resilience.

As we start the year, it is natural to reflect on 2025 performance and consider the trends that could shape the months ahead. The last year turned out to be an excellent one for investors around the globe. As of December, the S&P 500 looked set to post another double-digit return, international stocks were approaching a 30% gain, and even smaller stocks were logging respectable, if lagging, performance. Fixed income joined the party as high-quality taxable bonds returned more than 7% through November.

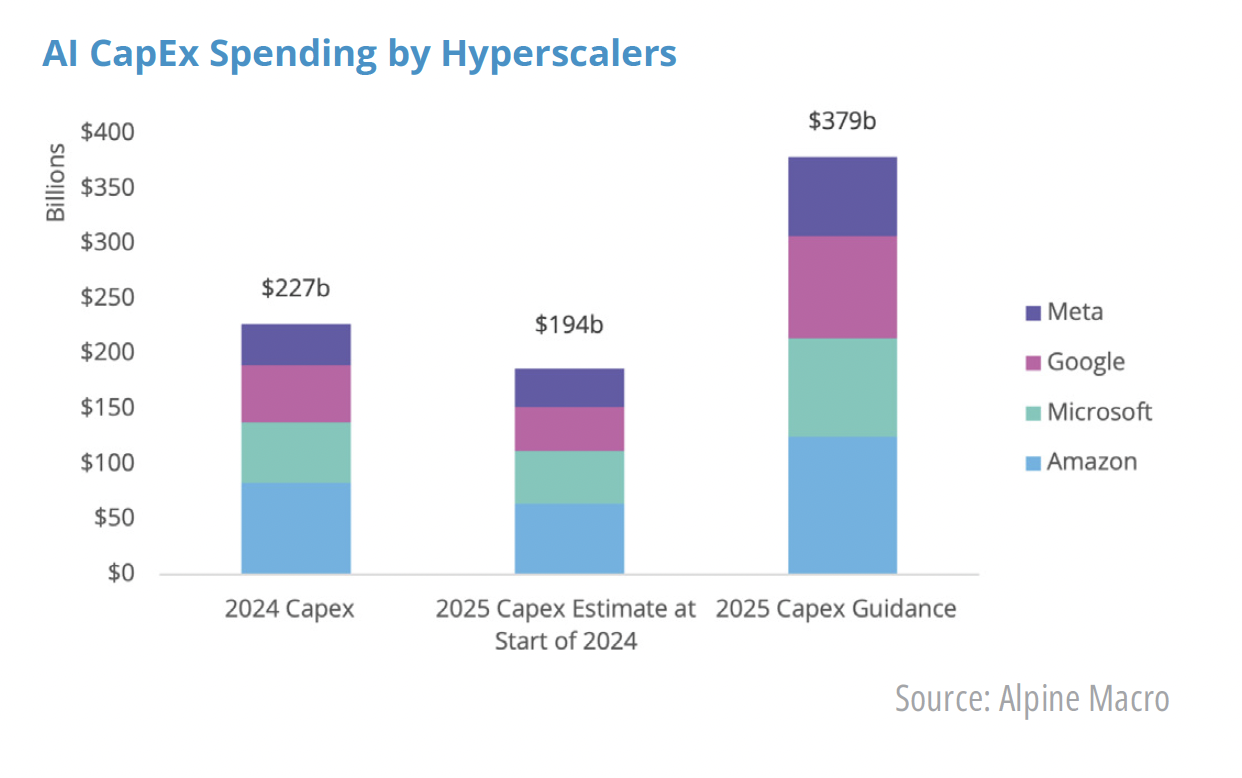

The first act of 2025 played out with far more drama than the final numbers suggest. A new administration arrived with tariffs and the DOGE program at the top of its agenda, overshadowing the administration’s efforts on tax cuts and deregulation. The unexpected policy announcements led the S&P 500 to approach bear market territory before going on to make new highs. It was a good reminder that markets usually digest political transitions reasonably well and shift their attention back to company performance. That happened again as Big Tech’s artificial intelligence (AI) spending, which could top $400 billion in 2026, quickly drowned out the political noise.

As we look ahead, there is no shortage of potential distractions that could create volatility in 2026.

This issue of Quarterly Insights covers key investment themes we expect to be top of investors’ minds.

Domestic Policies

Midterm years are historically the weakest of a presidential cycle, and the second year of a term has typically delivered the deepest correction. Investors will have plenty to fret about including taxes, spending, trade policy, and AI regulation. Yet the historical pattern also shows that recoveries following these corrections are just as robust. Long-term investors who can see through the political fog have usually been well rewarded.

A potential bright spot for markets is that consumers may experience a near-term sugar rush. The tax benefits of the One Big Beautiful Bill Act should hit bank accounts during the 2025 tax filing season, with estimates suggesting more than $517 billion in refunds. That is a 44% increase over 2025 and could give consumption a timely boost in the first quarter.

Though as we’ve said before, these tax benefits will mostly impact a wealthy few, while stripping critical services for many. We encourage our clients to consider donating these tax “savings” back to services now in dire need of funding. Watch our Tax Planning: Impact in Dollars & Values video here!

Federal Reserve Policy

With inflation above the Federal Reserve’s target and growth slowing, the central bank faces a delicate balancing act: supporting a cooling job market without reigniting price pressures. The Federal Open Market Committee has become more fractured as dissenters push for tighter and looser policy. It is not a great sign when the committee charged with steering the economy cannot agree on which direction the wheel should turn.

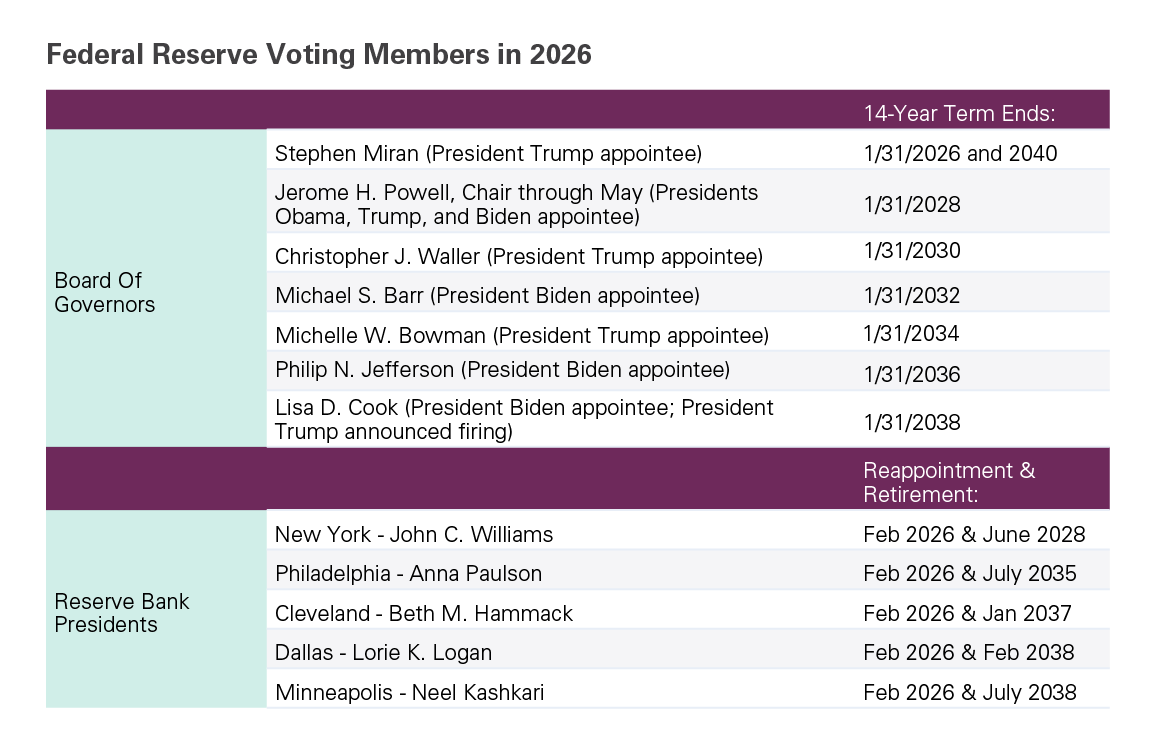

On top of that, 2026 could bring the biggest reshaping of the Fed since the financial crisis. With Chair Jerome Powell’s term ending in May and uncertainty surrounding Governor Lisa Cook’s position, five of the seven board seats could become Trump appointees. Five reserve bank presidents are also up for reappointment. The result could be a central bank with a very different philosophical makeup at a time when policy is already at a crossroads.

Credit Cracks

Private credit has enjoyed a golden era as borrowers sought speed and certainty while investors chased higher, floating-rate yields. The market has grown rapidly as a result, but the tone is beginning to shift. The Fed has flagged the asset class as a vulnerability, but it has also noted that the diversity of lenders reduces the systemic risk compared to the old bank dominated model.

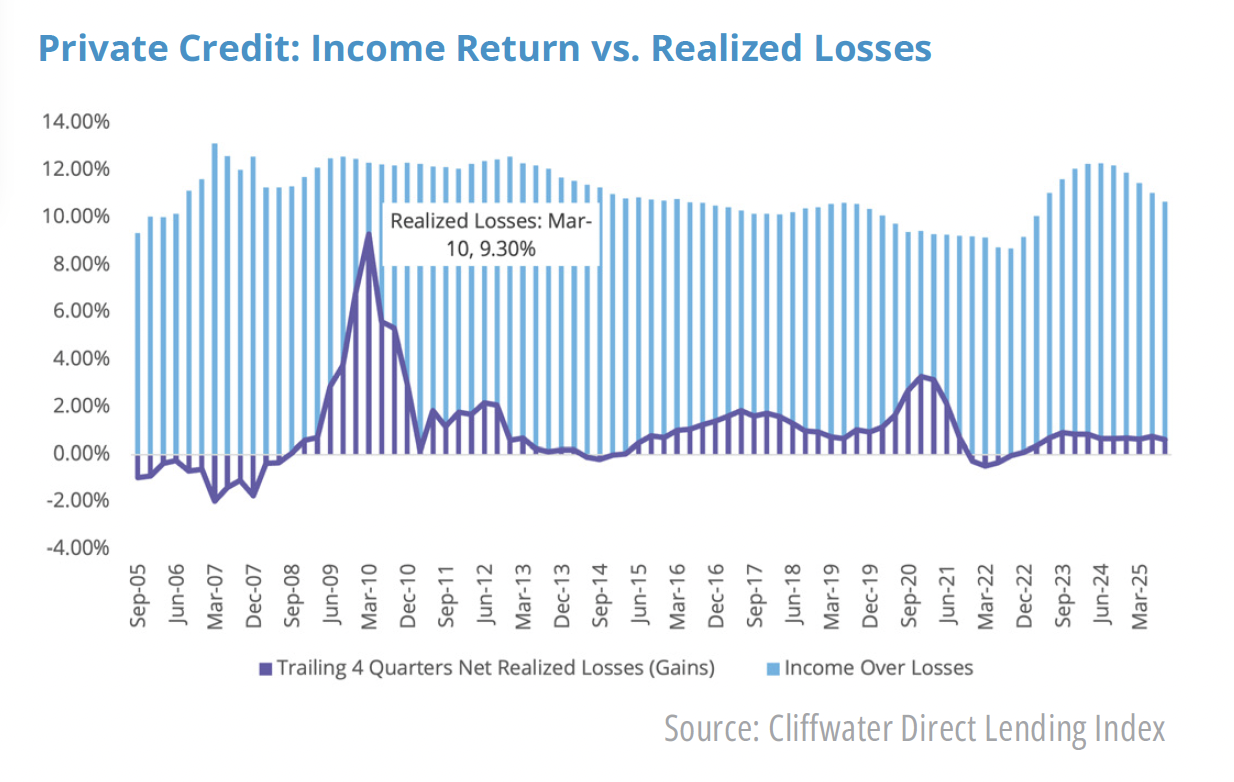

Recent headlines about private credit have made some investors understandably skittish about the potential for outsized losses. It helps to remember that private credit is primarily an income-driven strategy rather than a price appreciation strategy. Historically, that income has been the main driver of total returns.

Even in the worst 12-month stretch of the financial crisis, realized losses reached 9.3% while income was 12.3%, leaving a positive spread of just over 3%. In other words, losses would need to climb well above crisis-era levels before income would fail to offset them.

At the same time, the ecosystem looks different today. The market is much larger, underwriting can vary across managers, and fair value marks can create more visible mark-to-market swings. That combination does not necessarily imply worse long-term outcomes, but it does raise the potential for greater volatility, making manager selection and diversification even more important.

AI Becomes a Show Me Story

Perhaps the most important risk and opportunity for markets in 2026 is the evolution of AI from a capital expenditure story to a results story. It has been easy to generate excitement over proofs of concept and impressive demos. Next year may be the moment when investors demand more than promise. The question will shift from what AI might do to its realized impact.

That requires moving beyond chatbots and meme generation into tangible product innovations and measurable financial outcomes. Will 2026 be the year we see the first widely available full self-driving system? Will non-tech companies show they can grow revenue with the same or fewer employees? Can AI deliver margin expansion in sectors that have seen little innovation for decades?

The risk is two-sided. We have little doubt AI will deliver over time, but if product cycles or adoption rates disappoint, markets could struggle with impatience. Conversely, if the cycle exceeds expectations, the upside could be tremendous. General purpose technologies tend to follow the classic pattern of overestimating short-term impact and underestimating longterm transformation. AI looks increasingly like one of those technologies.

Want To Work With Us?

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third-party sources, which may become outdated or otherwise superseded without notice. Third-party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Total return includes reinvestment of dividends and capital gains. Mentions of securities are to demonstrate passive funds versus active funds, and low-cost funds. The mentions of specific securities should not be construed as recommendations of securities. Performance is historical and past performance is not an indication of future results. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements, or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability, or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this article. R-24-6678